Dr. Mary Campagnolo's patient had her diabetes well-controlled for years on a long-acting formulation of metformin. Then she switched insurance companies.

The new insurer required prior authorization for a medication she'd been taking successfully for years. Their demand: switch back to generic metformin, which had previously caused her significant gastrointestinal problems, to "prove" she needed the long-acting version. She needed to make herself sick to justify the medication that was already working.

Why the difference? Not new medical evidence. Just a different insurer with different rules.

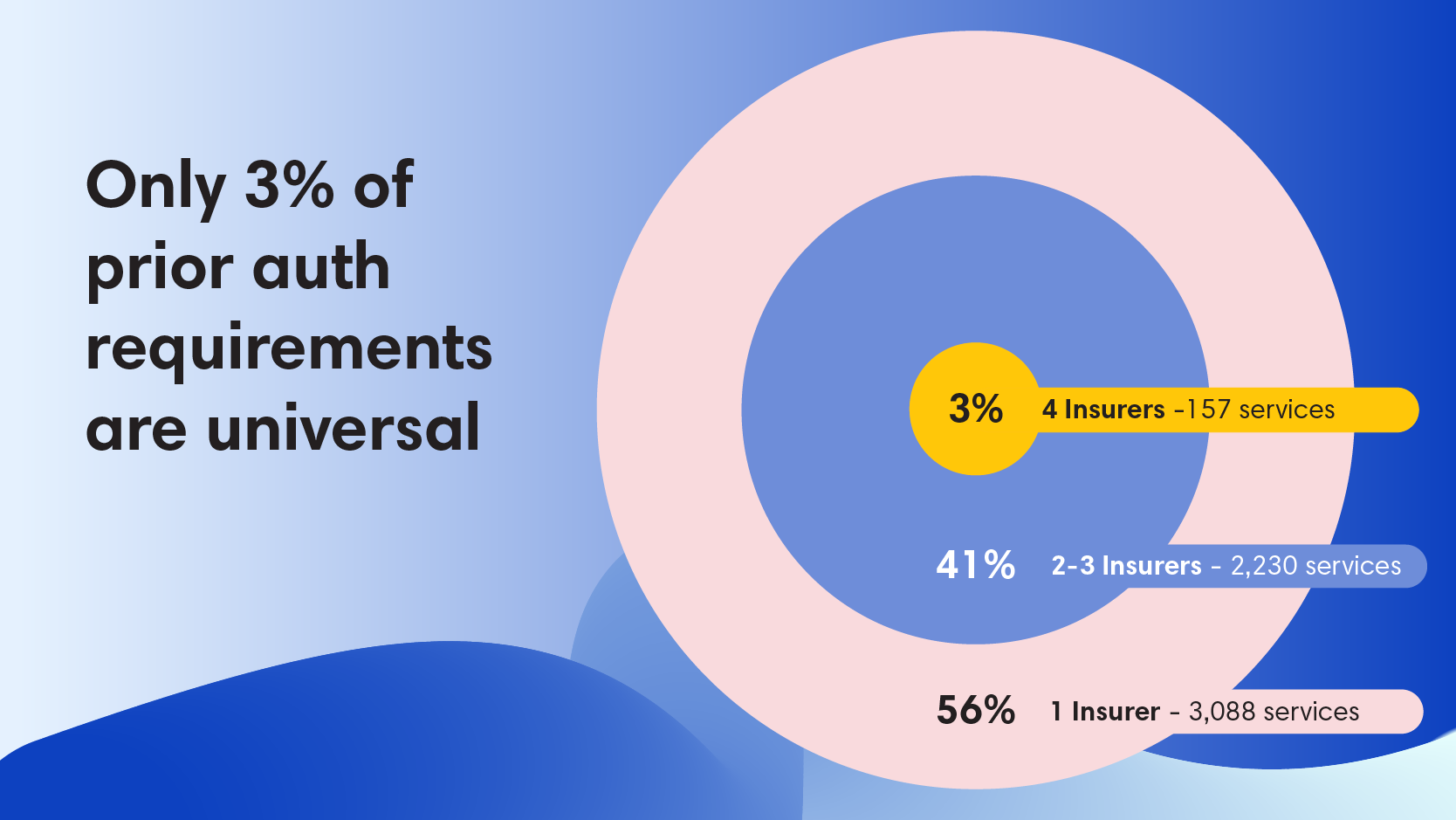

New research out of Stanford examined four major commercial insurers and found that only 3% of prior authorization requirements were consistent across all four plans.

Think about that:

- Out of 5,475 healthcare services requiring PA, only 157 had agreement

- More than half (56%) were unique to a single insurer

- Even for those 157 services where all insurers agreed PA was necessary, zero had identical criteria or requirements for approval

If clinical practice guidelines showed this little consensus, we'd question whether they were evidence-based at all. Insurers position prior authorization as a mechanism that ensures care is medically necessary and appropriate. But then wouldn't insurers agree (even half the time) about when it's needed?

This matters especially for self-funded employers. Unlike fully insured plans, you control your PA requirements. Your TPA's rules are recommendations, not mandates. More than half of all PA requirements exist at only one insurer.

Ask yourself:

- How many services does your plan require PA for?

- What's the clinical rationale behind each one?

- Which of your PA requirements have broad consensus, and which are unique to your TPA?

- And can you see where your healthcare dollars actually go?

Because with only 3% consensus across insurers, understanding what you've inherited matters more than ever.